IFRS STANDARD SETTING PROCESS

NOW THAT WE SEE HOW IMPORTANT IFRS IS TO MAKING THE WORLD AN INTEGRATED ECONOMY, LET'S SEE HOW IT IS DEVELOPED.

LET'S WATCH A VIDEO TO UNDERSTAND BETTER.

THE STEPS IN THE IFRS STANDARDS SETTING PROCESS HAVE BEEN DELINEATED BELOW.

- SETTING THE AGENDA

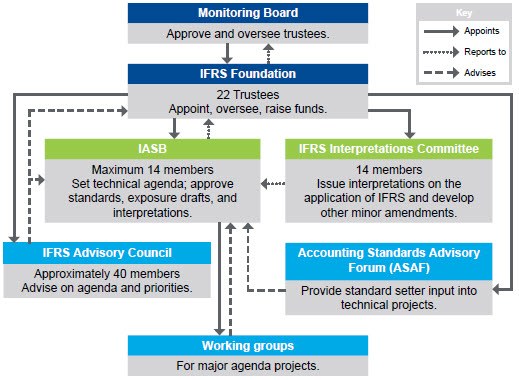

- THE INTERNATIONAL ACCOUNTING STANDARDS BOARD (IASB), DEVELOPS HIGH QUALITY FINANCIAL REPORTING STADARDS, SEEKING TO ADDRESS A DEMAND FOR BETTER QUALITY INFORMATION THAT IS OF VALUE TO THOSE USERS OF FINANCIAL REPORTS.

- IASB CONSIDERS THE FOLLOWING :

- RELEVANCE TO USERS OF THE INFORMATION

- THE RELIABILITY OF INFORMATION THAT COULD BE PROVIDED

- EXISTING GUIDANCE AVAILABLE

- POSSIBILITY OF INCREASING CONVERGENCE

- QUALITY OF THE IFRS TO BE DEVELOPED

- RESOURCE CONSTRAINTS

- STAFF REVIEWS AND RAISES ISSUES THAT MIGHT WARRANT IASB'S ATTENTION

- IASB DISCUSSES ON THE COMMENTS OF OTHER STANDARD SETTERS, IFRS ADVISORY COUNSIL, IFRS INTERPRETATIONS COMMITTEE, ETC

- CONSIDERATION OF CONVERGENCE INITIATIVES

- ALL DECISIONS MADE BY A MAJORITY VOTE AT A IASB MEETING

2. PLANNING THE PROJECT

- CHANGES TO BE ADDED IN THE ACTIVE AGENDA

- ALL CRITERIA TO BE MET FOR THE ITEM TO QUALIFY FOR INCLUSION IN ANNUAL IMPROVEMENTS

- AMENDMENTS FOLLOW THE SAME DUE PROCESS AS OTHER IASB PROJECTS

- PRIMARY OBJECTIVE - TO ENHANCE QUALITY OF IFRS

- IASB NOW ESTABLISHES A WORKING GROUP AND A PROJECT TEAM

- PROJECT MANAGER DRAWS UP A PROJECT UNDER SUPERVISION OF DIRECTORS OF TECHNICAL STAFF

3. DEVELOPING AND PUBLISHING THE DISCUSSION PAPER

- NORMALLY THE FIRST PUBLICATION BY IASB TO SOLICIT EARLY COMMENTS FROM CONSTITUENTS

- IT INCLUDES OVERVIEW OF THE ISSUE, POSSIBLE APPROACHES IN ADDRESSING THE ISSUE PRELIMINERY VIEWS OF THE AUHTOR AND INVITATION TO COMMENT

- DISCUSSION PAPERS WHICH ARE DRAWN BY OTHER STANDARD SETTERS ARE DISCUSSED IN IASB MEETINGS. IASB ALSO CHECKS THE APPROPRIATENESS OF ANALYSIS ON WHICH TO INVITE PUBLIC COMMENTS

- IASB PREPARES ITS DISCUSSION PAPERS IN CONSIDERATION OF THE RECOMMENDATIONS OF STAFF, IFRS ADVISORY COUNCIL, WORKING GROUPS, ETC

- GENERAL TIME LIMIT FOR ACCEPTING COMMENTS IS 120 DAYS, WHICH MAY BE FURTHER EXTENDED FOR MAJOR PROJECTS

- COMMENT LETTERS ARE POSTED ON THE IASB WEBSITE

- IASB MAY CONDUCT FIELD VISITS, PUBLIC HEARINGS OR ROUND TABLE MEETINGS FOR MORE INPUT ON AN ISSUE

4. DEVELOPING AND PUBLICATION OF EXPOSURE DRAFT

- SETS OUT SPECIFIC PROPOSAL IN THE FORM OF A PROPOSED IFRS

- IT IS PREPARED CONSIDERING STAFF RESEARCH AND RECOMMEDATIONS, COMMENTS RECEIVED ON DISCUSSION PAPER, SUGGESTIONS OF IFRS ADVISORY COUNCIL, WORKING GROUPS, ETC

- MINIMUM OF NINE VOTES IS NECESSARY TO PUBLISH AN EXPOSURE DRAFT FOR PUBLIC COMMENT

- A PERIOD OF 120 DAYS IS ALLOWED FOR COMMENT ON EXPOSURE DRAFT. IF MATTER IS URGENT, THEN A PERIOD OF NOT LESS THAN THIRTY DAYS IS ALLOWED FOR COMMENTS WITH THE PRIOR APPROVAL FROM 75% OF TRUSTEES

- IASB THEN REVIEWS THE COMMENT LETTERS AND RESULTS OF OTHER CONSULTATIONS

- IASB MAY CONDUCT FIELD VISITS, PUBLIC HEARINGS OR ROUND TABLE MEETINGS FOR MORE INPUT ON AN ISSUE

5. DEVELOPING AND PUBLISHNG THE STANDARD

- IFRS IS DEVELOPED IN THE IASB MEETINGS, AFTER CONSIDERATION OF COMMENTS ON THE EXPOURE DRAFT

- IASB CONSIDERS WHETHER TO EXPOSE REVISED PROPOSALS FOR PUBLIC COMMENT

- IASB PREPARES A PROJECT SUMMARY AND FEEDBACK STATEMENT, WHICH GIVE DIRECT FEEDBACK TO THE COMMENTS, IDENTIFY THE MOST SIGNIFICANT MATTERS RAISED IN COMMENTS AND IASB'S RESPONSE TO THOSE MATTERS

- IF IASB IS SATISFIED WITH THE CONCLUSION, IT INSTRUCTS THE STAFF TO DRAFT THE IFRS

- IFRS INTERPRETATIONS COMMITTEE REVIEWS A PRE-BALOT DRAFT

- BEFORE BALLOT, A NEAR-FINAL DRAFT IS PLACED ON THE WEBSITE FOR ITS PAID SUBSCRIBERS

- AFTER ALL ISSUES ARE RESOLVED, AND IASB MEMBERS BALLOTED IN FAVOUR OF PUBLICATION, IFRS IS ISSUED

- THIS IS FOLLOWED BY PUBLICATION OF ANY PROJECT SUMMARY, FEEDBACK STATEMENT AND ANY EFFECT ANALYSIS

6. AFTER THE STANDARD IS ISSUED

- POST ISSUANCE OF AN IFRS STANDARD, IASB MEMBERS HOLD REGULAR MEETINGS WITH INTERESTED PARTIES TO UNDERSTAND UNANTICIPATED ISSUES RELATING TO IMPLEMETATION AND POTENTIAL IMPACT OF ITS PROVISIONS

- CONSISTENCY IN APPLICATION OF IFRS IS ENSURED THROUGH EDUCATIONAL ACTIVITIES

- IASB CARRIES OUT POST IMPLEMENTATION REVIEW OF EACH NEW IFRS OR MAJOR AMENDMENTS, LIMITED TO IMPORTANT AND CONTENTIOUS ISSUES

- REVIEWS ARE ALSO CARRIED OUT DUE TO CHANGES IN FINANCIAL REPORTING ENVIRONMENT AND REGULATORY REQUIREMENTS, ADVERSE COMMENTS ON QUALITY OF IFRS

- IASB CONDUCTS INFORMAL CONSULTATIONS THROUGHOUT THE IMPLEMENTATION OF THE IFRS OR AMENDMENT

Comments

Post a Comment